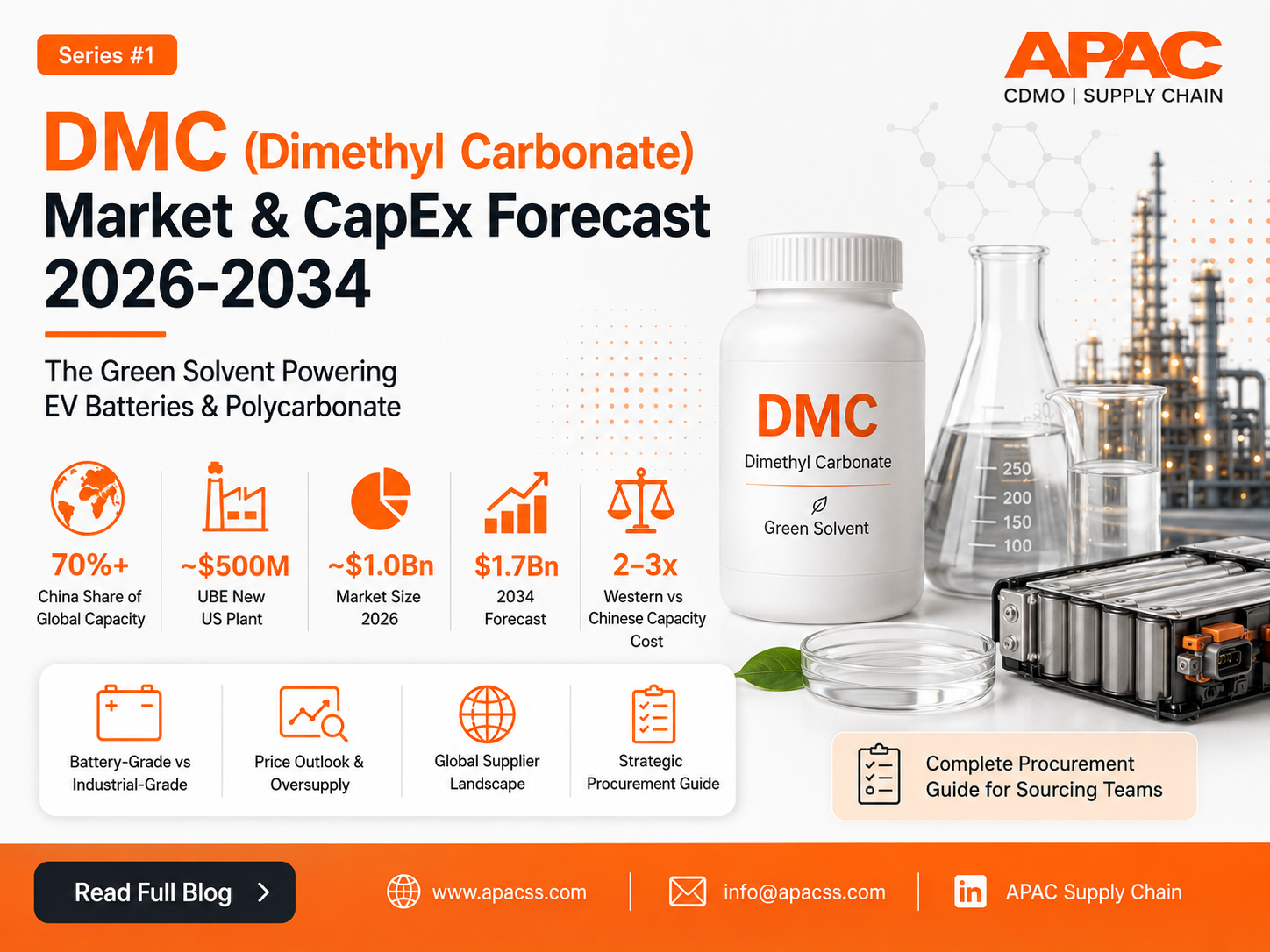

Dimethyl Carbonate (DMC) CapEx Forecast 2026: Market Size, Capacity & Price Outlook & Strategic Procurement Guide

⚡ Capacity cycle in motion: China holds 70%+ of global dimethyl carbonate capacity, and the market is currently oversupplied — prices have been flat since 2024. At the same time, capacity is globalising for the first time: UBE's ~$500M battery-grade DMC plant in Louisiana starts up in 2026. For procurement teams, this is a buyer's-leverage window that will not stay open indefinitely.

In brief: Dimethyl carbonate (DMC, CAS 616-38-6) is the non-toxic, biodegradable carbonate ester that is both the workhorse solvent in lithium-ion battery electrolytes and the phosgene-free route to polycarbonate. The global DMC market sits at roughly $1.0–1.9 billion depending on source, with battery-grade the fastest-growing segment. A wave of capacity investment — led by China and now spreading to the US and Europe — is reshaping who can supply what, and at what cost. This guide gives procurement professionals, battery-material buyers and polycarbonate manufacturers everything they need to know and act on now.

1. What Is Dimethyl Carbonate (DMC)?

Most people have never heard of dimethyl carbonate — yet it sits inside the two most important industrial stories of the decade: the electric-vehicle battery boom and the shift to safer, greener plastics. Supply chain professionals need to understand what they are actually buying, and why a major capacity cycle is about to reshape its availability and price.

Dimethyl carbonate (DMC) is a carbonate ester (CAS 616-38-6) produced primarily from methanol. It is non-toxic, biodegradable and exempt from VOC classification in several jurisdictions, which has made it a flagship “green chemistry” molecule. It works as a methylating and carbonylating agent — replacing toxic phosgene and methyl halides — and as a high-performance, low-viscosity solvent.

Key fact for procurement teams: Battery-grade and industrial-grade DMC are effectively two markets with two price curves and two risk profiles. Treating them as one commodity is the most common and most expensive mistake in DMC sourcing — the purification step that separates them is also the single biggest driver of plant cost.

2. The 2026 Market Picture: Two Megatrends, One Molecule

The DMC market is being pulled by two structural demand engines at once — and reshaped by a capacity response that is, for the first time, going global. Three forces define the 2026 picture.

The structural read: Demand for DMC is rising on durable, regulation-backed trends — but in the base case, 2026–2030 adds more new capacity than incremental demand. That keeps buyer leverage strong in commodity and industrial grades, while battery-grade qualification barriers and localisation policy create defensible premium niches.

3. Global Market Size & Forecast 2025–2034

Published DMC market estimates diverge widely — by a factor of two to three — depending on whether they count merchant-only or total (including captive) volumes, and how they treat the battery-grade premium. Rather than cherry-pick a single headline, the table below shows the full spread so procurement teams can anchor on the range, not one number. Where possible, anchor on volume.

| Research Source | Base Value | Forecast | CAGR |

|---|---|---|---|

| MarketsandMarkets (2025) | $1.94 Bn (2025) | $3.29 Bn by 2030 | 11.1% |

| Fortune Business Insights (2026) | ~$1.0 Bn (2026) | $1.73 Bn by 2034 | 7.1% |

| Global Market Insights (2024) | $1.1 Bn (2023) | 8.2% CAGR to 2032 | 8.2% |

| The Business Research Co. (2026) | $1.18 Bn (2025) | $1.51 Bn by 2029 | 6.4–6.9% |

| Transparency Market Research (2025) | $0.6 Bn (2024) | $1.1 Bn by 2035 | 5.6% |

On a volume basis — the more reliable lens for CapEx planning — the global market was estimated at roughly 2.06 million tonnes in 2023, growing at around 6.9% per year (Prismane Consulting). Asia-Pacific dominates demand with somewhere between 41% and 60% of the global total depending on definition, with China the single largest producer and consumer.

Why the estimates differ so much: A merchant-market view counts only DMC sold between companies; a total-market view also counts captive volumes consumed inside integrated polycarbonate or electrolyte plants. Battery-grade material commands a premium that inflates value-based sizings. For procurement decisions, tonnes and regional capacity balances matter more than any single dollar figure.

4. DMC Price Trajectory: Oversupply and the Buyer's Window

Unlike a shortage-driven market, DMC enters this CapEx cycle from a position of oversupply. Understanding the price environment is essential for procurement teams modelling cost exposure — and for spotting where leverage currently sits.

| Period | Price Environment | Driver |

|---|---|---|

| 2024 (full year) | Stagnant / soft | High Chinese inventories; weak Western battery & polycarbonate demand |

| Q4 2024 | Region-split volatility | APAC firmer on battery demand; North America / Europe under oversupply pressure |

| Q1–Q3 2025 | Subdued, rebounds distant | Cautious procurement; persistent overhang; competitive Asian imports |

| Late 2025 (battery grade, China) | ~$745–800 / tonne | Delivered-to-factory battery-grade benchmark |

| Late 2025 (industrial grade, China export) | ~$430–650 / tonne | Volume export offers; economies of scale |

DMC production cost tracks methanol, which in turn tracks crude and natural gas. With methanol feedstock broadly available and energy prices subdued through 2025, production economics stayed neutral — reinforcing the oversupply-driven pricing trend. Regional pricing disparities persist: Chinese suppliers offer the lowest prices on economies of scale, while European and North American prices typically run 20–30% higher on logistics and compliance costs.

Procurement implication: For industrial-grade DMC, buyers are operating in a market priced near cash cost for non-integrated producers. That is exactly the environment to negotiate quality upgrades and longer-term, methanol-indexed agreements — while battery-grade economics depend on qualification premiums and regional supply security rather than spot spreads.

5. The CapEx Wave: Who Is Building and When It Arrives

New DMC capacity is being built across three continents — but the strategic story is not just how much, it is where and at what cost. The most consequential shift is that world-scale, battery-grade capacity is being built outside China for the first time.

| Company / JV | Investment | Location | Timeline | Notes |

|---|---|---|---|---|

| UBE Corporation | ~$500 Million | Waggaman, Louisiana, USA | Start-up 2026 | 100,000 t/y DMC + 40,000 t/y EMC; first world-scale battery-grade unit in North America; downstream PCD/PUD planned |

| BASF | €100 Million (reported) | Ludwigshafen, Germany | 2025–26 | Reported expansion of existing DMC capacity; verify against primary BASF release |

| Jiangsu Sailboat × Asahi Kasei | Not disclosed | Lianyungang, China | Live Dec 2024 | CO₂-feedstock EC + DMC using Asahi Kasei licensed technology; high-purity battery grade |

| SABIC × LG Chem | Not disclosed | TBD | Announced Nov 2024 | Strategic collaboration to produce DMC for the lithium-ion battery market |

| Chinese producers (aggregate) | ~$2 Billion tracked | Shandong, Fujian, others | 2021–2027 | Mostly transesterification; battery-grade share rising; tracked by Industrial Info Resources |

The CapEx read: China's roughly $2 billion of tracked projects continues to expand a capacity base that is already oversupplied, while the West adds its first world-scale battery-grade units. The base-case outcome for 2026–2030 is more new capacity than incremental demand — with utilisation, not nameplate, deciding which plants thrive.

6. Global Supplier Landscape: Where DMC Is Made Today

For buyers, the supplier map is diversifying — which is good news. Below is a practical view of where credible DMC capacity sits today, by region and role.

- Shida Shenghua

- Shinghwa Advanced Material

- Shandong Wells (S-Sailing)

- Henan GP Chemicals

- 70%+ of global capacity

- Integrated methanol feedstock

- UBE Corporation

- Asahi Kasei (CO₂ tech licensor)

- Leading non-Chinese battery-grade tech

- UBE also building in the US

- High-purity EMC integration

- UBE (Louisiana) — 2026 start-up

- Eastman Chemical

- LyondellBasell

- Huntsman

- First domestic battery-grade anchor

- IRA-aligned supply security

- BASF (Ludwigshafen)

- SABIC (Spain)

- SABIC × LG Chem JV

- Net importer of battery grade today

- Compliance-driven cost base

- No world-scale battery-grade yet

- Import-served demand today

- PLI-linked cell build-out rising

- Most likely next greenfield 2027–30

- Key watch item for buyers

- Import-served, FDI-driven

- Following cell-capacity investment

- Logistics-advantaged for regional buyers

- Watch for offtake-backed projects

7. Capital Intensity & the Cost Structure of a DMC Plant

Understanding what it costs to build DMC capacity explains the entire competitive map — and why a Western tonne is not the same as a Chinese tonne. For a greenfield plant, total installed capital cost decomposes roughly as follows (based on published plant cost models).

| Cost Component | Share of Total CapEx | Notes |

|---|---|---|

| Site acquisition & preparation | 5–8% | Preference for petrochemical complexes for feedstock integration; safety buffer zones |

| Raw material storage & handling | 10–15% | Methanol tankage, inert blanketing, vapour recovery; stainless product tanks for battery grade |

| Reaction & separation (ISBL core) | 40–50% | Reactors and distillation trains; battery-grade purification is the biggest cost delta |

| Utilities & offsites (OSBL) | 15–20% | Steam, power, cooling, effluent; CO/oxygen handling for carbonylation routes |

| Engineering, EPC & contingency | 15–20% | Higher for first-of-a-kind CO₂ routes |

Indicative Capital Intensity (Modelled Estimates)

Using UBE's disclosed Louisiana investment as the one solid Western anchor (~$500M for 140,000 t/y combined carbonates, i.e. roughly $3,500–3,600 per annual tonne), the indicative ranges below follow. These are modelled estimates, not quoted project costs.

| Plant Archetype | Indicative CapEx (US$/t/y) | Basis |

|---|---|---|

| China, industrial grade, brownfield | ~$800–1,400 | Low EPC, existing utilities, co-product credits |

| China, battery grade, integrated | ~$1,500–2,500 | Adds purification train and clean utilities |

| US / EU, battery grade, greenfield | ~$3,000–4,000 | UBE Louisiana anchor; Western EPC, labour & compliance premium |

The 2–3x rule: A Western battery-grade tonne of DMC capacity costs roughly two to three times more capital than a Chinese tonne. Western projects are therefore viable mainly where qualification barriers, tariffs, logistics or localisation policy (IRA / EU battery rules) secure a durable price premium or anchor offtake. This single ratio explains why China leads and why Western capacity needs policy support to clear.

8. Strategic Procurement Guide: 4 Actions for Procurement Teams Right Now

The DMC market gives buyers something the base-oil market does not: leverage. But that leverage is grade-specific and time-bound. Here are the four actions procurement teams should take now.

The window is grade-specific. For industrial grade, time is on the buyer's side — negotiate hard. For battery grade, the window to qualify and lock terms is open now and starts closing as Western capacity tightens balances from 2027. The teams that act on both simultaneously will outperform those treating DMC as a single commodity.

9. How APAC Supply Chain Supports DMC & Industrial Chemical Procurement

APAC Supply Chain is a global chemical and industrial sourcing partner, connecting verified international buyers with quality-certified manufacturers and suppliers across China, Japan, India, South Korea and broader Asia-Pacific — the heart of global DMC production.

Start Your DMC Supplier Qualification

Tell us your grade (battery or industrial), target market, and volume requirements. We will come back within 48 hours with verified supplier options.

✉ Email Our Team Explore apacss.com →10. Frequently Asked Questions

Dimethyl carbonate (CAS 616-38-6) has two flagship uses: as the workhorse solvent in lithium-ion battery electrolytes (battery grade) and as the phosgene-free route to polycarbonate (industrial grade). It is also used as a green methylating and carbonylating agent, a low-VOC solvent in paints and coatings, and in adhesives, pharmaceuticals, agrochemicals and fuel additives. It is non-toxic and biodegradable, which is why it is replacing toxic phosgene across multiple processes.

Estimates diverge by two to three times. Fortune Business Insights values the market near $1.0 billion in 2026 rising to about $1.7 billion by 2034 (~7.1% CAGR), while MarketsandMarkets puts it at $1.94 billion in 2025 rising to $3.29 billion by 2030 (11.1% CAGR). On a volume basis the market was about 2.06 million tonnes in 2023 growing near 6.9% per year. The wide spread reflects merchant-versus-total scope and battery-grade premiums — for procurement, volume and regional capacity balances are more reliable than any single value figure.

DMC prices have been broadly flat since 2024 because new Chinese capacity outpaced demand, creating a persistent inventory overhang. Weak Western battery and polycarbonate demand and competitive Asian imports added downward pressure. In late 2025, battery-grade DMC traded around $745–800 per tonne in China, while industrial-grade export offers were reported as low as $430–650 per tonne at volume. This oversupply makes 2026–2028 a buyer's-leverage window, especially for industrial grade.

China dominates with over 70% of global capacity and producers such as Shida Shenghua, Shinghwa Advanced Material, Shandong Wells (S-Sailing) and Henan GP Chemicals. The biggest new investments are UBE's ~$500 million, 100,000 t/y DMC plus 40,000 t/y EMC plant in Louisiana (start-up 2026), a reported BASF Ludwigshafen expansion, the Jiangsu Sailboat CO₂-feedstock plant using Asahi Kasei technology (live December 2024), and a SABIC–LG Chem battery-DMC collaboration announced in November 2024. Industrial Info Resources has tracked roughly $2 billion of DMC projects across China.

Industrial-grade DMC is typically 99.0–99.5% pure and serves polycarbonate, solvents, coatings, adhesives and fuel additives. Battery-grade DMC requires 99.99%+ purity with ppm-level water and metal limits and is used as a lithium-ion electrolyte solvent and as the feedstock for EMC. The intensive purification train needed for battery grade is the single biggest capital-cost difference between the two grades, and qualification at cell makers can take 12–24 months.

A Western battery-grade DMC tonne of capacity costs roughly two to three times more to build than a Chinese tonne. Using UBE's disclosed Louisiana investment as an anchor (about $3,500–3,600 per annual tonne for an integrated battery-grade complex) against indicative Chinese brownfield industrial-grade costs of roughly $800–1,400 per annual tonne, the gap reflects higher Western EPC, labour, utilities and compliance costs. Western projects are viable mainly where qualification barriers, tariffs or localisation policy secure a durable premium or anchor offtake.

In the base case, 2026–2030 is expected to add more new DMC capacity than incremental demand, particularly in industrial grade where Chinese additions have already outrun consumption. This keeps buyer leverage strong and creates utilisation risk for plants ramping into soft prices. Battery-grade is more protected because qualification barriers, regional supply-security value and offtake-backed projects limit who can serve that segment.

For international DMC procurement, documentation should include: a Certificate of Analysis (CoA) per batch confirming purity, water content, and metal limits (critical for battery grade); Certificate of Origin (CoO); Safety Data Sheet (SDS / MSDS); Technical Data Sheet (TDS); REACH compliance documentation for EU shipments; and customs HS code classification. For battery-grade material destined for cell makers, electrolyte-qualification records and tighter ppm-level specifications are also required. APAC Supply Chain provides full documentation packages for all qualified suppliers in our network.

11. Conclusion

Dimethyl carbonate has moved from a niche green solvent to one of the most strategically contested specialty chemicals in the global supply chain. It sits at the intersection of the EV-battery and green-polycarbonate megatrends — and a major capacity cycle is now redrawing the map of who can supply what, and at what cost.

The fundamentals are clear: a market worth roughly $1–2 billion depending on definition, battery-grade as the fastest-growing segment, prices flat on a Chinese-led oversupply, world-scale Western capacity arriving for the first time via UBE's Louisiana plant, and a capital-intensity gap that makes a Western tonne cost two to three times a Chinese one. For procurement and supply chain professionals, the message is grade-specific but unambiguous: industrial-grade buyers hold the leverage today, while battery-grade buyers must qualify and lock terms before Western capacity tightens balances from 2027.

Companies that treat DMC as two distinct markets — not one commodity — and act in 2026 while the oversupply window is open will be significantly better positioned through the capacity cycle ahead.

If you are reviewing your dimethyl carbonate sourcing strategy — whether for battery electrolytes, polycarbonate, coatings, or industrial solvents — we welcome the conversation. Reach out to our team at ibd@apacss.com or explore our full industrial chemical and sourcing portfolio at www.apacss.com.