Strait of Hormuz Crisis 2026: How Chemical & Pharma Supply Chains Are Breaking Down — And Where GCC Buyers Are Sourcing Now

Strait of Hormuz Closure 2026: The Full Impact on Chemical & Pharma Supply Chains

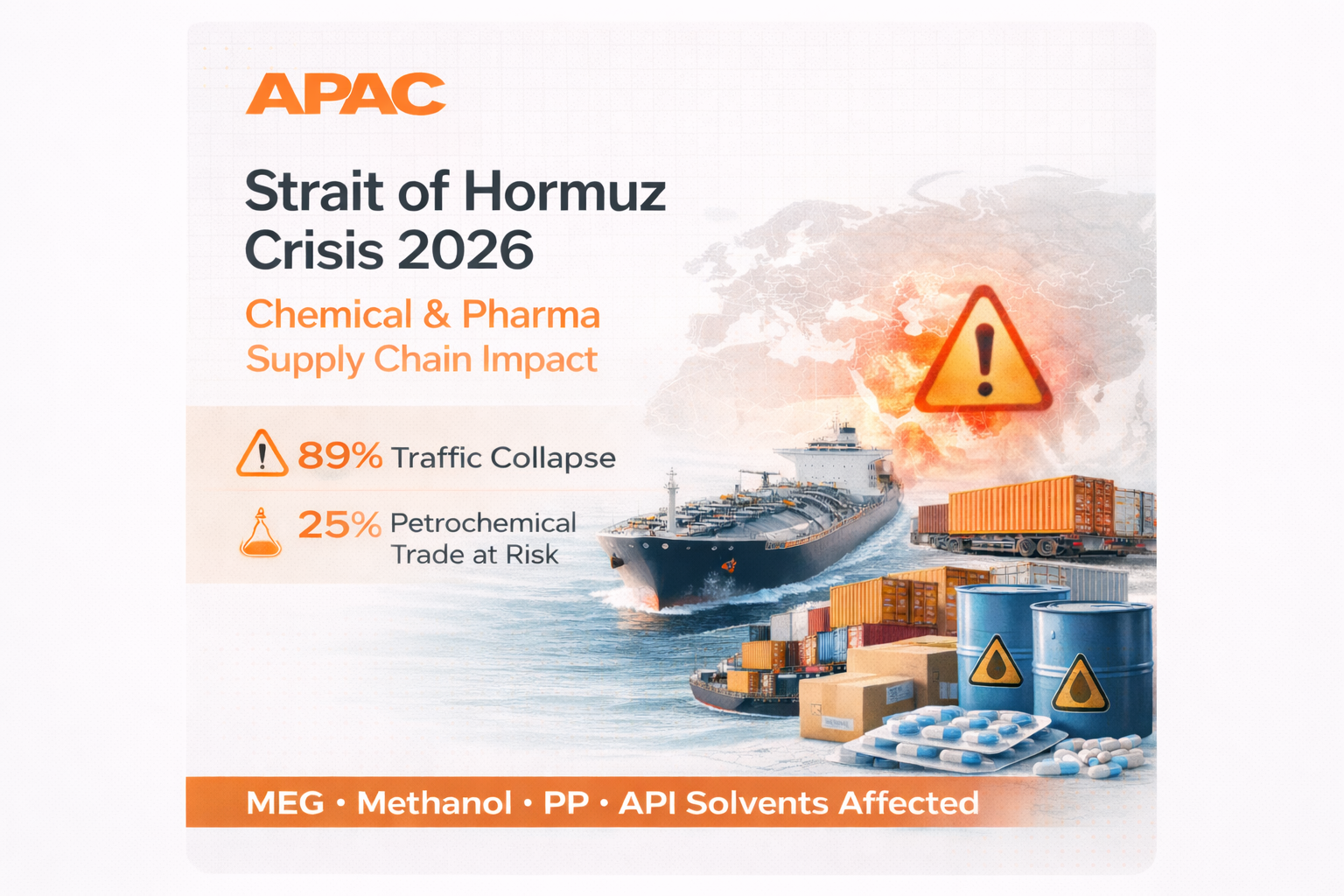

From MEG and polypropylene to API solvents and ammonia — what the 89% traffic collapse means for procurement, pricing, and where supply is actually moving.

On April 10, 2026, Iran capped traffic through the Strait of Hormuz at 15 ships per day — down from a pre-conflict average of 138. That single restriction has disrupted roughly 20% of global oil supply and 25% of the world's petrochemical trade. For chemical and pharma procurement professionals, this is not a downstream geopolitical event. It is a direct upstream supply shock.

Why the Strait of Hormuz Is the World's Most Critical Chemical Corridor

The Hormuz Strait is a 21-mile passage between Iran and Oman. Before the current conflict, 138 ships transited it daily — carrying crude oil, LNG, petrochemical feedstocks, fertilisers, and finished chemicals to markets across Asia, Europe, and beyond.

The IEA's 2025 data places approximately 25% of the global petrochemicals market as Hormuz-dependent for either feedstock sourcing or finished product shipment. The EIA confirms that 84% of all Hormuz-routed crude flows to Asian markets.

Which Chemicals Are Directly Disrupted?

The disruption is not limited to crude oil. The Gulf region — particularly Saudi Arabia, the UAE, and Qatar — supplies significant volumes of petrochemical feedstocks and finished chemicals to Asian and global markets. The following products are at active supply risk:

MEG (Monoethylene Glycol)

MEG is one of the most critically affected products. The WEF reported 6.5 million tonnes of MEG shipped through Hormuz in 2025. Qatar's Ras Laffan Industrial City — the world's largest petrochemical complex — halted all polymer, methanol, and urea production on March 2, 2026. MEG buyers in textile, PET packaging, and antifreeze manufacturing are facing immediate tightening.

Polypropylene & Polyethylene

Saudi Arabia and the UAE are major PP and PE exporters to Asian and African markets. With restricted shipping, contract fulfilment rates have dropped sharply. Buyers dependent on Gulf-origin PP for packaging, automotive, or medical applications are the most exposed.

Methanol

Iran is one of the world's largest methanol producers. The conflict has both disrupted Iranian export volumes and restricted transit of non-Iranian methanol through Hormuz. Pharma-grade methanol and industrial methanol for formaldehyde production are both affected.

Ammonia & Urea

Gulf producers supply a significant share of global ammonia and urea, especially to South and Southeast Asian agricultural markets. Fertiliser manufacturers and industrial users (refrigerants, water treatment) face tightening supply and rising prices.

Impact on the Pharmaceutical Supply Chain

The pharma sector's exposure is often underappreciated in commodity-focused analysis. Several key API solvents and pharma intermediates have Hormuz-linked supply chains:

- Methanol — used as solvent in API synthesis and chromatography. Gulf methanol disruption directly impacts pharma-grade availability.

- Acetic Acid — feedstock for aspirin, paracetamol, and a wide range of pharmaceutical intermediates. Gulf acetic acid producers are operating under logistics constraints.

- Ammonia — used in the manufacture of nitrogen-containing APIs and as a pH adjuster in drug formulation.

- Phenol — precursor to disinfectants, analgesics, and antiseptics. Any Gulf supply tightening affects phenol derivative pricing globally.

- Urea (pharma grade) — used in dermatological and wound-care formulations. Supply from Gulf-linked producers has tightened.

The Real Cost Impact: What Procurement Is Facing Right Now

- Feedstock price increase of 15–25% on petrochemical inputs under sustained disruption (IEA scenario modelling).

- Lead time extension of 10–14 days for vessels rerouting via the Cape of Good Hope — increasing working capital requirements and stock buffer needs.

- War risk insurance surge from 0.125% to 0.2–0.4% per transit — adding $250,000+ per VLCC voyage, costs that pass through to chemical buyers.

- Force majeure invocations from Gulf chemical producers citing conflict conditions — invalidating existing supply contracts.

- Asian resin shortages projected within weeks by Sparta Commodities and other industry analysts.

India's Position: Why It Is a Structural Alternative

India's response to the Hormuz disruption has been rapid and structural — not temporary. As of March 2026 (MoPNG data), India has rerouted 70% of its crude imports away from Hormuz. Indian refineries are running on diversified crude, and Indian chemical manufacturers are operating at full capacity with domestic feedstock supply chains that are largely insulated from Hormuz risk.

Government Policy Supporting Indian Chemical Supply

The Government of India exempted key petrochemical feedstocks from customs duty until June 2026 to maintain domestic manufacturing competitiveness. Products covered include PP, PE, PVC, PET, methanol, and ammonia. This directly supports Indian manufacturers' ability to price competitively for export.

No Gulf routing. No war-risk premium. No ceasefire dependency.

What Chemical & Pharma Professionals Are Searching Right Now

The following are the high-traffic search terms being used by procurement and supply chain professionals in the GCC and Asia in response to this crisis.

| Search Term | Volume Trend | Buyer Profile |

|---|---|---|

| MEG shortage 2026 | ↑↑ Surging | MEG buyers, textile & packaging |

| polypropylene price increase 2026 | ↑↑ Surging | Plastics & packaging procurement |

| methanol supply disruption Gulf | ↑↑ Surging | Pharma & industrial buyers |

| ammonia shortage 2026 | ↑ Rising | Fertiliser & industrial gas buyers |

| Hormuz closure chemical industry | ↑↑ Surging | All chemical procurement |

| API solvent shortage GCC | ↑ Rising | Pharma manufacturers GCC |

| India chemical supplier UAE | ↑ Rising | Procurement diversification |

| petrochemical feedstock alternative Gulf | ↑ Rising | Commodity procurement |

| naphtha price spike 2026 | → Steady | Refinery & cracker operators |

| force majeure chemical contract 2026 | ↑ Rising | Legal & procurement teams |

| Indian manufacturer GCC distributor | ↑ Rising | Distributor sourcing teams |

Procurement Action Plan for GCC Chemical Buyers

Audit your Gulf-origin raw material exposure immediately

Map every SKU to its country of origin. Flag products where Gulf supply accounts for more than 40% of your procurement volume — these are your highest-risk lines in the next 30–60 days.

Review supplier force majeure clauses now

Gulf producers are already invoking force majeure. Understand your contractual position and begin documenting supply shortfall evidence for any insurance or commercial claims.

Open parallel sourcing channels from India

Indian manufacturers for PP, PE, MEG, methanol, API solvents, and pharma intermediates are operating at full capacity. The window to secure allocation is narrow — establish supply relationships before spot market pressure fully hits.

Rebuild buffer stock for critical inputs

If your standard lead time is 30 days, plan for 45–50 days given Cape rerouting additions. Increase safety stock targets for your most critical raw materials by at least 30%.

Lock pricing on Indian-origin materials before the market reprices

Indian manufacturer pricing has not yet fully reflected the Hormuz risk premium that Gulf-origin materials are carrying. This arbitrage window is temporary — act in the next 2–4 weeks.

Frequently Asked Questions

Conclusion

The Hormuz crisis is not a temporary freight disruption. It is a structural shock to global petrochemical and pharma raw material supply chains that will take months to normalise — even under optimistic ceasefire scenarios. For GCC chemical and pharma buyers, the procurement window to secure non-Gulf supply is narrow and narrowing.

Indian manufacturers represent the most immediately accessible, competitively priced, and logistics-resilient alternative for GCC markets — with no Hormuz routing dependency, full production capacity, and government policy tailored to support export competitiveness through mid-2026.

Discuss your sourcing requirements

APAC Sourcing Solutions connects verified Indian chemical & pharma manufacturers with GCC distributors. Drop an enquiry at apac-sourcing.com or connect with Alok Srivastava on LinkedIn. We respond within 24 hours.